The other day when I included a link to Tom Luongo's musings on Secession I had intended to include more commentary of my own. However, I was put off by my ignorance of economic matters. A day or so later I'm just as ignorant as before, but I still want to raise these issues to see what others--who may know more--have to say.

One article on Secession that I came across while I was preparing the blog Recommended Reading For Christmas contended that Blue counties account for 70% of GDP and that Red counties are basically populated by losers who scuffle to get by and have little to offer the country as a whole. That seemed a pretty extreme assessment to me. I mean, I knew that the Blue counties don't actually produce much of anything--not energy, not food, not really too much in terms of consumer goods. Still I wasn't sure how to proceed.

Many of you, I'm guessing, have some familiarity with Charles Hugh Smith through republication of his blogs at Zerohedge. If so, you'll know that his big bugaboo is the "financialization" of our economy. As far as that goes, I've always been receptive to the idea that the decline and repeal of Glass Steagall is what got us to where we are now, with an economy that's top heavy in the financial sector and a population that keeps falling further behind.

Obviously, to that extent I blame simple minded Libertarians for enabling the pass we've come to. Luongo, a self professed Libertarian, at least recognizes that the "American Myth" of Classical Liberalism has pretty much collapsed and doesn't have much to offer in terms of a way forward for the nation. Trump wanted to restructure the economy, away from financialization and towards productivity in the real world, and we're seeing the result--a Deep State hit and the collapse of our constitutional order. I think we all get that: While the top 5% of the population wasn't out there stuffing the ballot boxes--they had useful idiots to do that--they were the ones who dictated that Trump had to go, constitution be damned.

Now, I can't say that I read everything that Smith writes--actually, far from it. Still, I decided that one way to proceed would be to see if I could find a blog in which he explains his ideas, excerpt that, and see what other conservatives might think of his thesis. My reason for doing this is because, while I acknowledge my ignorance in this regard, it seems that any attempt to make sense of what's coming at us in the tunnel ahead will have to take financialization into account.

With that as my premise, I dug up this blog:

TUESDAY, JULY 28, 2020

The Nation Is Falling Into the Abyss Between Wall Street and Main Street

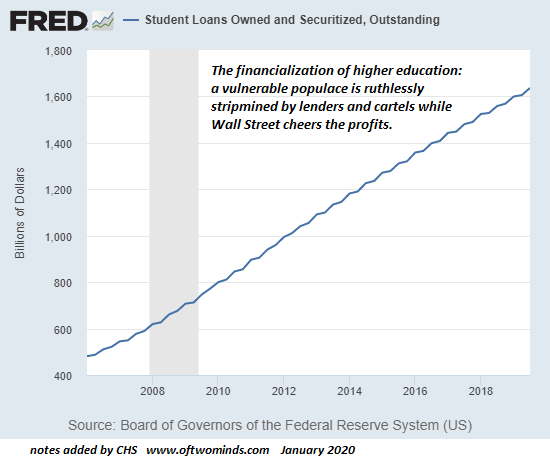

I know this runs counter to every dominant narrative, but a vaccine doesn't really matter, opening up doesn't really matter, and the size of the "free money" stimulus checks doesn't matter.What matters is that the nation is falling into the abyss that's opened between Wall Street and Main Street, and nothing will stave off the collapse of the social order other than a fundamental re-ordering of the way we create and distribute money and political power, as money buys political influence.The last economic tide with widespread benefits to Main Street was 30 years ago. Since then, the Federal Reserve and other central banks have incentivized globalization and financialization, two dynamics that favor mobile capital and financier skims and scams.... Financialization has given those with access to central bank credit ways to skim great wealth from the system without creating any value whatsoever.Financialization isn't a consequence of having capital: it's the consequence of having access to unlimited central bank credit, ...Leveraging phantom collateral is another feature of financialization. ...Financialization is not about investing in productive enterprises; it's all about skimming wealth while providing no value to the real economy or society.The hidden toxin in financialization is the resulting concentration of wealth can buy concentrations of political power. ... Once the politicos are in your pocket, the regulators and judiciary fall into line or are marginalized by new statutes or gutted budgets....One example is the student loan "industry," which prior to financialization did not exist. ...That the exploited class of students have little to no income and no guarantee of income doesn't matter. What matters is a previously unexploited asset can be turned into debt that can be sold at an immense profit.And so student loan debt has skyrocketed from near-zero to $1.6 trillion in less than a generation. ...Globalization and financialization have been the two engines of soaring wealth inequality. ...In other words, globalization is the result of those at the top of the wealth-power pyramid shifting borrowed capital around the world to exploit lower costs of labor, commodities, environmental regulations and taxes.This manifests as offshoring of jobs, the stripmining of forests, minerals, etc., the degradation of local ecosystems, the decline of tax revenues derived from capital and the explosive rise in stock market valuations as wages stagnate or decline.A key element in globalization is the transfer of risk from the owners of capital to the workers and public resources. ...Alas, all good predations end when the prey has been dragged to the ground and consumed. ......Main Street has been in slow-motion collapse for a generation, but this terminal decay was masked by hyper-financialization and debt-fueled spending by consumers who became accustomed to filling the widening gap between their income (stagnant) and the costs of their lifestyle (rising), as they chased the top 5% who benefited from globalization and financialization.Debt creates the warm and fuzzy illusion of wealth, but at a cost: debt payments never disappear, but income and profits can slide effortlessly to zero.

...

To be continued, I think.

You won't find much discussion of this among "mainstream" conservatives, but this analysis dovetails quite nicely with discussions about the grave evil of "usury" in Catholic Social Teaching (as far as back as the Middle Ages). Usury is "the charging of any interest on a loan simply by virtue of the loan contract, that is, without any other justifying cause except that money is being loaned". (source for the quote: https://distributistreview.com/archive/is-usury-still-a-sin).

ReplyDeleteSurprisingly, and on a side note, I learned that Keynes agreed with the Catholic Church on this point (see here: http://distributism.blogspot.com/2009/03/its-all-about-usury.html).

Thanks for the reference. Re Keynes:

Delete"What Keynes is saying in this somewhat technical language is that when returns to pure loans are higher than returns to actual investments, you will have a problem; if you can make more money lending to consumers at 25% than to auto makers at 10%, then the money for making things will dry up, and loans will shift to consumption and speculation."

I have a lefty friend who laughed up his sleeve while informing me of the high GDP levels of the urban / Democrat archipelago versus "JesusLand." Of course, being an former educator he has no idea how GDP is calculated. When I asked him why NYC's and Silicon Valley's GDP were high, he mumbled something about financial markets and iPhones.

ReplyDeleteAbout 40 years ago, a keynote speaker at an American Production and Inventory Control Society (APICS) conference I attended asked the crowd to consider the meaning of a "service economy" in the absence of a solid manufacturing base. Any economy not primarily based on producing goods is essentially parasitical--and also a house of cards. Silicon Valley and NYC can keep their phony GDP. They will have trouble eating ad clicks and collateralized debt obligations.

That 'farmers' strike' thing surfaced on Limbaugh last week. The bad news: someone has to finance the collection and processing of all that food, not to mention the production of all that the Rust Belt produces--and the purchases of those products.

DeleteIt's not a simple task to pull those teeth.

Of course, I get the role of capital in producing food for mass consumption. However, there is an irreducible, more essential resource required than capital. Cooperatives of farmers could survive on their land. Cooperatives of Javascript coders and software product managers would be reduced to marauding bands of looters in months--if not weeks.

DeleteFarmer co-ops 'survice.' OK. What about the NON-twits--like e.g., our blog-host here--who also like to eat regularly but who live in Big City? Get a password to meet Farmer Brown at I-55 and I-80?

DeleteNot saying it can't be done, but this is a lot more complicated than Monopoly.

I recommend int'l finance blogger FoFoA on various $$ things, incl. on how an excess *amount* of usury/ financialization can stagnate/ destabilize an otherwise fruitful/ sustainable situation:

ReplyDelete"Re-lending is fine and normal to a degree. That degree is where it is done professionally, with one's *own surplus* revenue.

Where it becomes hazardous is, when it is done systemically and *passively*, by savers who leave it up to someone else, to determine the lending standards.

All of this money circulates in the same pool, so using credits as the system's reserves, and the passive savings of virtually everyone in the world, crowds the banks and professional investors within the financial and monetary arena.

This crowding pushes the banks and professional investors into *riskier* and more questionable activities, in order to make a living.

The result is low interest rates (because there is too much money competing for a limited pool of credible borrowers), lower lending standards (because passive money is being managed by people who make an up-front percentage, and then have no more *skin in the game*), low inflation (because the process itself systematically overvalues the currency, on an ongoing and cumulative basis), and economic stagnation (once debt and malinvestment levels reach a certain point of saturation).

That's where we are today, in my view, on a global scale.

Money hoarded as savings or foreign reserves must find a vehicle to be hoarded into.

This creates a massively oversized and passively generic demand, for *debt and equity* investment vehicles, which leads to bubbles, malinvestment, debt saturation, across-the-board unprofitability, and ultimately to persistent economic stagnation, where uneconomic and unprofitable businesses continue operating at a loss, just to service their debt, and in some cases where government stimulus is involved, just to keep people employed. We see this happening everywhere today, even in China.

It is a vicious feedback loop, and it only gets worse as the viability of new products becomes secondary, to their corporate presence in the investment markets.

One of the main criticisms of the secular stagnation hypothesis, which I mentioned earlier, is that innovation and growth in the IT sector is underappreciated by economists.

But just consider how many of the new rising *stars in the tech* industry are more about the business of selling shares, than creating real economic value.

In essence, global *savings* (because in the $IMFS, "savings" is defined as money hoarding) has outstripped profitable investment opportunities.

There are more "savings" in the world today, than there are truly-economic opportunities to make a profit, therefore the very act of saving for the future today worsens imprudent lending standards, inflates valuation bubbles in overpriced (and therefore unprofitable) industries, and promotes the illusion of new rising stars of productivity, like Pets.com and Candy Crush.

In supply and demand terms, there is too much savings, relative to investment opportunities that are profitable due to real economic value creation.

The return on "savings" (interest in the case of debt, and dividends or profits in the case of equity) is low, because there is too much supply (savings) relative to demand (profitable opportunities).

These are exactly the conditions in which *bubbles* arise—when "savings" or investment capital are in overabundance...."

From http://fofoa.blogspot.com/2014/12/global-stagnation.html?commentPage=3 .

My clarification of his abbreviation: $IMFS = Int’l Monetary Fund System (run for $US).

Well, that's certainly interesting.

DeleteFor those of you who didn't check out the whole article posted above, FoFoA refers there to famous economists (Summers, Krugman, Greenspan) who concede that global stagnation is real.

DeleteTo overcome this stagnation, FoFoA urges that such passive savings be encouraged to move, from crowding into esoteric vehicles, into simple (and often more stable) vehicles, like gems, gold, cases of vintage wine, classic cars, and other "precious" objects.

DeleteOf such "precious" objects, gold is the most fungible/ liquid, since each (1/10 oz.) gold coin is as salable as any other, to all-but the poorest of people, all over the globe.

And, such coins are very durable/ hide-able, even *keyster*-able.

That would impose a discipline on the monetary system that would be most unwelcome to the speculative class.

Delete"unwelcome to the speculative class."

DeleteYeah, that's likely why they so oppose DJT, who FoFoA sees as a threat to them.

For some references to related issues, see

https://fofoa.blogspot.com/search?q=trump&max-results=20&by-date=true , esp. the post "Hyperinflation'll Fix That", about DJT vs. MMT.

Instead of "My clarification of his abbreviation: $IMFS", I should've put "his acronym".

ReplyDeleteA barter system would be plausible in rural areas. Three chickens to have a tooth filled, four with anesthesia. :)

ReplyDeleteA batter system has a limit literally the length of your arm. Obtaining filling mat'l, novacaine, dental tools, the labor to maintain some semblance of hygiene, sooner or later, probably sooner unless the goal is to live in a tiny village circa 1100 A.D., barter has to translate to something fungible.

DeleteTom S.